Why should I start investing?

Harness the power of investing

The goal of investing is to grow your money over time. Although investing has inherent risk, it also has the potential for greater returns than if you simply left your money in a bank account.

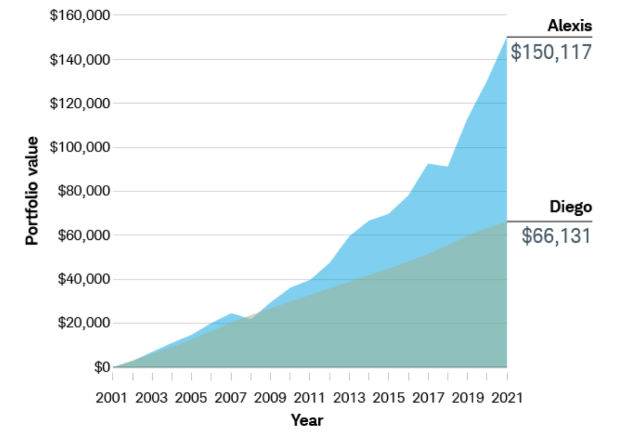

The saver: Diego

Diego put away $3,000 per year into a bank account. He invested using 3-month Treasury bills. While the interest rate was relatively low, his funds were safe and easily accessible. At the end of 20 years, his funds grew to $66,131.

The investor: Alexis

Alexis also set aside $3,000 per year, but she invested her funds into a moderate portfolio over 20 years. At the end of 20 years, her funds grew to $150,117.

The power of compounding

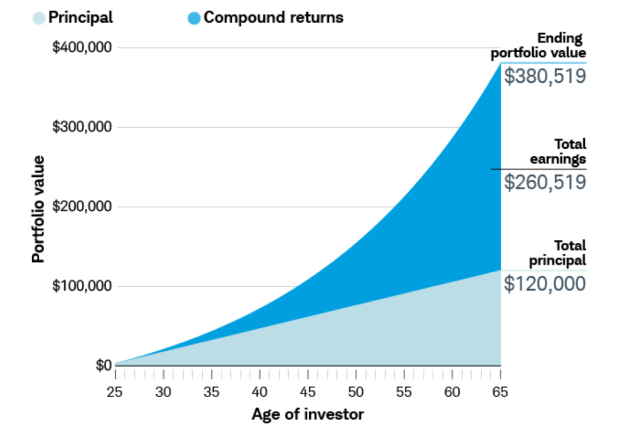

Investing isn't just about how much money you have to invest. It's also about how much time you have to invest it. That's because of the power of compound growth.

Compound interest makes your money grow faster because interest is calculated on the accumulated interest over time as well as on your original principal. Compounding can create a snowball effect, as the original investments plus the income earned from those investments grow together.

If Alexis keeps investing $3,000 per year for 40 years with an average annual return of 5%, watch how her balance skyrockets over time. At the end of 40 years, her portfolio is worth $380,519, even though the actual principal she invested was only $120,000. Every year, her 5% return was based on a newer, larger balance comprising her initial investment, subsequent yearly investments, and the money she earned from interest. That's the power of "compound returns."

Don't forget about inflation

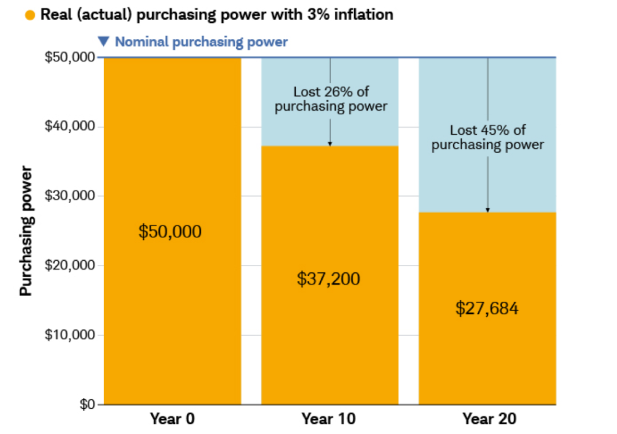

There's another big factor to consider when comparing savings to investing. Recent savings rates haven't kept up with the rate of inflation, meaning the actual purchasing power of money in a savings account can shrink over time.

This chart illustrates the impact of inflation on the purchasing power of a fixed annual $50,000 income. Here we see that with a hypothetical 3% inflation rate, the fixed annual $50,000 income can purchase only $37,200 worth of goods or services at the end of 10 years (a 26% loss of purchasing power) and only $27,684 worth of goods or services at the end of 20 years (a 45% loss of purchasing power).

How to invest: Five-step guide to help set yourself up for success

This actionable guide can help you create an investment strategy that aligns with your goals.

Have questions? We're here to help.

-

Call

CallIf you live in the U.S., call 800-654-2593.

If you live outside the U.S., visit the Contact Us page to find your country's local number.

Our specialists are available Monday through Friday, 24 hours a day.

-

Chat

ChatLog in to your account, head to the Equity Awards tab, and select the chat icon to be connected directly with a Stock Plan Services Specialist.

-

Access resources

Access resourcesHave questions about navigating your equity account? Searching for a specific form?

Visit our Videos & Forms page for helpful resources.